SumUp vs Zettle UK is a comparison many small business owners make when choosing a card payment provider. Both providers offer simple pay-as-you-go card payment solutions designed for small businesses. Neither requires a long-term contract. Both allow businesses to start accepting card payments quickly, and both are popular choices among sole traders, market traders and independent retailers.

However, there are some important differences.

SumUp charges a slightly lower standard transaction fee than Zettle and offers an optional reduced-rate pricing plan that can significantly lower costs for some businesses. While both providers offer a range of card payment solutions, SumUp provides more choice when it comes to standalone payment devices and offers optional reduced-rate pricing through Payments Plus.

Zettle, now part of PayPal Point of Sale, remains a strong option thanks to its simple pricing structure and close integration with the PayPal ecosystem.

Based on pricing, SumUp is likely to offer better overall value. However, businesses that already rely heavily on PayPal may still prefer Zettle.

In this guide, we’ll compare fees, hardware, software, payouts and overall value to help you decide which provider is the better fit for your business.

If you’re comparing providers, you may also find our guides to Best Card Payment Machines UK, Cheapest Card Readers UK, Card Machine Fees Explained, SumUp Fees UK, Square Fees UK, Zettle Fees UK, Dojo Fees UK and Square vs SumUp UK helpful.

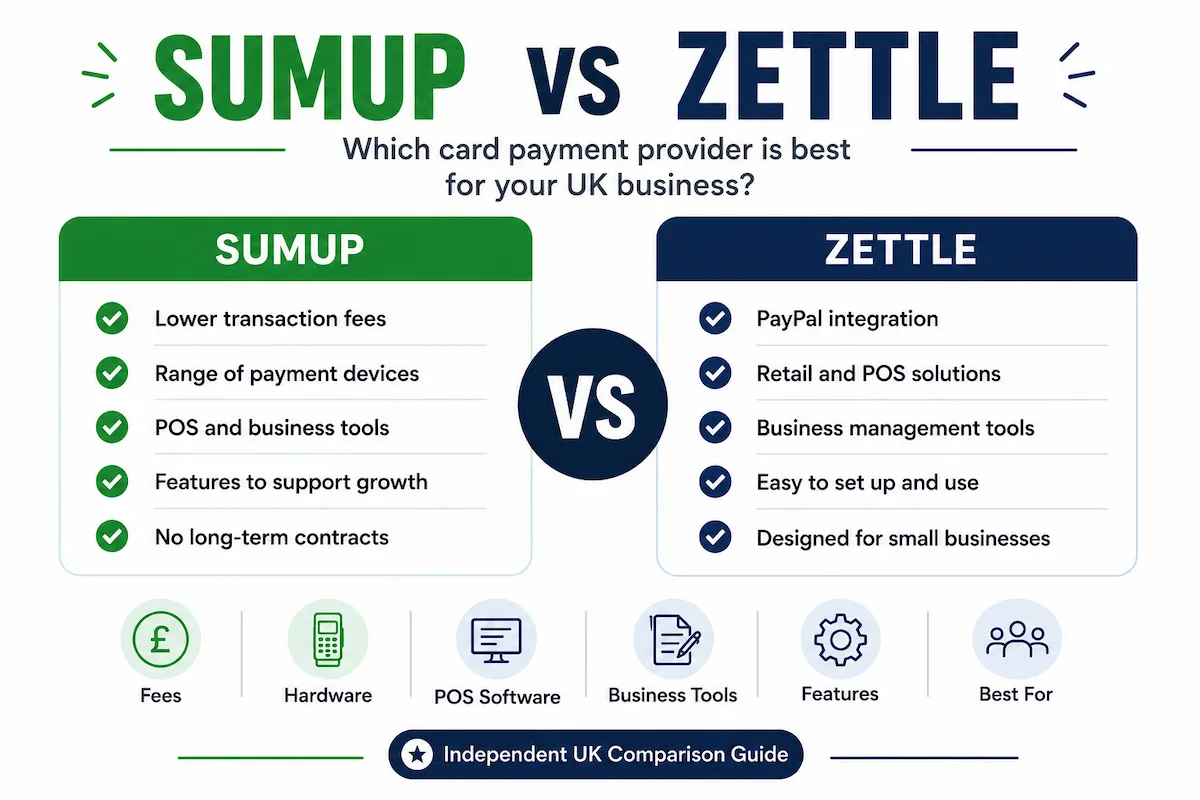

💡 SumUp vs Zettle UK at a Glance

SumUp

✓ Lower standard transaction fee (1.69%)

✓ Optional reduced-rate pricing through Payments Plus

✓ Broader range of payment devices

✓ No monthly fee required

✓ Suitable for both small and growing businesses

Zettle

✓ Simple pay-as-you-go pricing

✓ Strong PayPal integration

✓ No monthly fee required

✓ Easy setup process

✓ Popular with small businesses and sole traders

Disclosure: Some links on this page are affiliate links. If you choose to purchase through them, we may earn a commission at no additional cost to you. Our comparisons and recommendations are based on independent research and editorial judgement.

Quick Verdict

If you’re researching SumUp vs Zettle UK, the quick verdict below highlights the key differences between the two providers.

Choose SumUp if:

- You want the lowest transaction fees.

- You process larger card payment volumes.

- You want access to a wider range of card readers and payment terminals.

- You want the option of reducing fees through Payments Plus.

- You expect your business to grow over time.

View SumUp pricing →

Choose Zettle if:

- You already use PayPal regularly.

- You want a simple pricing structure.

- You want to keep your payment services within the PayPal ecosystem.

- You want an easy-to-use card payment solution without additional pricing plans.

View Zettle pricing →

Based on pricing, SumUp comes out ahead thanks to its lower fees and optional reduced-rate pricing. Zettle remains a strong alternative for businesses already invested in the PayPal ecosystem.

SumUp vs Zettle UK Comparison Table

📱 Viewing on mobile? Swipe left and right to see the full table.

| Feature | SumUp | Zettle |

|---|---|---|

| In-person transaction fee | 1.69% | 1.75% |

| Monthly fee required | No | No |

| Reduced-rate pricing available | Yes (Payments Plus) | No |

| Long-term contract | No | No |

| Tap to Pay | Yes | Yes |

| Entry-level card reader | Solo Lite | PayPal Reader |

| Range of payment devices | Broader range | Reader and StoreKit focused |

| Online payments | Yes | Yes |

| POS software | Yes | Yes |

| Inventory management | Yes | Yes |

| PayPal integration | No | Yes |

| Suitable for growing businesses | Excellent | Good |

| Best for | Overall value and flexibility | PayPal users |

📌 Quick Summary

Based on pricing, SumUp comes out ahead thanks to its lower transaction fees, optional reduced-rate pricing and broader range of payment devices. Zettle’s main differentiator is its connection to the PayPal ecosystem, which may appeal to businesses already using PayPal.

Which Is Cheaper?

At first glance, there is not a huge difference between SumUp and Zettle’s standard transaction fees.

SumUp charges 1.69% for in-person card payments, while Zettle charges 1.75%.

For businesses processing only a small amount of card payments each month, the difference is relatively minor. However, as transaction volumes increase, even small differences in percentage fees can add up over time.

SumUp also offers an additional advantage through its Payments Plus plan, which can reduce transaction fees on eligible domestic consumer card transactions to as little as 0.99%.

Because Zettle does not currently offer an equivalent reduced-rate option, SumUp generally becomes more cost-effective as card payment volumes grow.

In the next section, we’ll compare the fees in more detail and look at how much each provider could cost your business each month.

Fees Comparison

For many businesses, transaction fees are one of the most important factors when choosing a card payment provider.

Both SumUp and Zettle use simple pay-as-you-go pricing with no monthly fee required, making them accessible to startups, sole traders and small businesses. However, there are some key differences that become more important as card payment volumes increase.

Standard Transaction Fees

SumUp charges a flat transaction fee of 1.69% for in-person card payments.

Zettle charges 1.75% for in-person card payments.

While the difference may appear small, SumUp is slightly cheaper on every transaction processed.

For example, on a £100 card payment:

- SumUp fee: £1.69

- Zettle fee: £1.75

That’s a difference of just 6p per transaction, but the savings can add up over hundreds or thousands of transactions throughout the year.

Reduced-Rate Pricing

One of SumUp’s biggest advantages is its optional Payments Plus plan.

For a monthly subscription fee, eligible domestic consumer card transactions can qualify for reduced rates from 0.99%, significantly lower than the standard 1.69% rate.

This can make a substantial difference for businesses that process large volumes of card payments each month.

Zettle currently does not offer an equivalent reduced-rate pricing plan, meaning businesses remain on the standard 1.75% transaction fee regardless of processing volume.

For lower-volume businesses this may not matter much, but for growing businesses the potential savings available through SumUp can be significant.

Monthly Cost Examples

The examples below use each provider’s standard pay-as-you-go transaction fee.

📱 Viewing on mobile? Swipe left and right to see the full table.

£2,000 per Month in Card Sales

| Provider | Monthly Fees |

|---|---|

| SumUp | £33.80 |

| Zettle | £35.00 |

Difference: SumUp saves approximately £1.20 per month.

£8,000 per Month in Card Sales

| Provider | Monthly Fees |

|---|---|

| SumUp | £135.20 |

| Zettle | £140.00 |

Difference: SumUp saves approximately £4.80 per month.

£20,000 per Month in Card Sales

| Provider | Monthly Fees |

|---|---|

| SumUp | £338.00 |

| Zettle | £350.00 |

Difference: SumUp saves approximately £12.00 per month.

Pricing correct at the time of writing. Providers may change fees, products, features or promotions over time.

Which Provider Offers Better Value?

Looking only at the standard transaction fees, the difference between SumUp and Zettle is relatively modest.

However, SumUp consistently comes out slightly cheaper, and the gap widens further for businesses that can benefit from Payments Plus and its reduced transaction rates.

For businesses processing only occasional card payments, pricing is unlikely to be the deciding factor.

For businesses taking thousands of pounds in card payments each month, SumUp’s lower fees and reduced-rate options give it a clear advantage.

Hardware Comparison

Both SumUp and Zettle offer modern card payment solutions designed for small businesses, but their hardware ranges take slightly different approaches.

Both providers offer hardware suitable for small businesses, but SumUp provides a broader range of standalone payment devices, while Zettle focuses on its PayPal Reader, StoreKit solutions and retail POS ecosystem.

Entry-Level Options

Both providers offer Tap to Pay, allowing businesses to accept contactless card payments directly on a compatible smartphone without purchasing a separate card reader.

For businesses that only take occasional card payments, this can be the cheapest way to start accepting cards.

Both providers also offer affordable entry-level card readers.

SumUp Solo Lite is designed as a low-cost portable card reader suitable for sole traders, market traders and mobile businesses.

PayPal Reader performs a similar role within the Zettle ecosystem and is designed for businesses wanting a straightforward card payment solution.

For most small businesses, either option will comfortably handle day-to-day card payments.

Hardware for Growing Businesses

As businesses grow, they often want more than a simple card reader. They may require:

- Faster checkout experiences

- Dedicated payment devices

- Countertop payment setups

- Integrated receipt printing

- More advanced point-of-sale systems

Both SumUp and Zettle offer solutions designed for growing businesses. However, SumUp provides a broader range of payment devices, including:

- Solo Lite

- Solo

- Solo + Printer

- Terminal

This gives businesses more choice when selecting hardware and can make it easier to find a setup that matches their specific requirements as they grow.

Retail and Hospitality Businesses

Retail shops, cafés and hospitality businesses often require more robust payment setups than mobile businesses or sole traders.

Both SumUp and Zettle offer solutions designed for retail environments, including POS software, inventory management tools and hardware suitable for countertop use.

However, SumUp provides a broader range of payment devices, including options such as the Solo Lite, Solo, Solo + Printer and Terminal. This gives businesses more flexibility as their payment requirements evolve.

For example, a small market trader may be perfectly happy using a simple card reader, while a busy café may prefer a dedicated payment terminal with integrated features and faster checkout processes.

🏆 Hardware Verdict

If you only need a simple card reader or Tap to Pay solution, there is little to separate the two providers.

However, SumUp offers more standalone payment devices and more choice as business requirements grow.

Winner: SumUp

Software & Features

While transaction fees and hardware often get the most attention, the software tools offered by a payment provider can also have a significant impact on day-to-day business operations.

Both SumUp and Zettle provide more than just card payment processing. They each offer a range of tools designed to help businesses manage sales, track inventory and accept payments through multiple channels.

SumUp Software

SumUp has expanded beyond card readers in recent years and now offers a broader business ecosystem than many people realise.

Available tools include:

- POS Lite

- Online Store

- Invoicing

- Payment Links

- Booking tools

- Gift Cards

- Payments Plus

For many small businesses, the included POS Lite software will be sufficient for basic retail and hospitality requirements.

Businesses that grow over time can also access additional tools without needing to change provider, making SumUp an attractive long-term option.

Zettle Software

Zettle’s software offering focuses on simplicity and ease of use.

Key features include:

- POS app

- Product library

- Inventory management

- Sales reporting

- Payment links

- PayPal integration

The software is straightforward to learn and provides most of the features that small businesses require for day-to-day operations.

For many sole traders and independent retailers, Zettle’s simpler approach may actually be an advantage, particularly if they only need basic point-of-sale functionality.

Online Payments

Both providers allow businesses to accept payments online as well as in person.

This can be useful for businesses that:

- Take deposits

- Sell through social media

- Accept remote payments

- Send invoices to customers

Neither provider requires a separate merchant account, helping to keep setup simple.

🏆 Software Verdict

For basic payment acceptance and point-of-sale functionality, both providers perform well.

However, SumUp offers a broader range of business tools and provides a clearer path for businesses that want to expand their payment and sales systems over time.

Winner: SumUp

Payouts & Payments

Receiving your money quickly is just as important as taking payments in the first place.

Both SumUp and Zettle provide straightforward settlement processes, but there are some differences worth considering.

SumUp Payouts

When customers make card payments through SumUp, funds are transferred directly to your linked bank account.

For most businesses, this provides a simple and familiar process with no additional steps required.

Businesses can easily track transactions through the SumUp app and dashboard, making it straightforward to monitor payments and settlements.

Zettle Payouts

Zettle also transfers funds to your linked business bank account, but its biggest advantage is its connection to the wider PayPal ecosystem.

Businesses that already use PayPal for online sales may appreciate having card payment services provided by the same company.

For some businesses, this can simplify administration and create a more connected payment setup.

PayPal Integration

One of Zettle’s key differentiators is its connection to the wider PayPal ecosystem.

If your business already relies heavily on PayPal, choosing Zettle may feel like a natural extension of systems you already use.

For example:

- Existing PayPal users

- Online sellers

- Small ecommerce businesses

- Businesses already familiar with PayPal tools

may find the integration appealing.

For businesses that rarely use PayPal, however, this advantage is much less significant.

Which Provider Has Better Payouts?

For most businesses, there is little practical difference between SumUp and Zettle when it comes to receiving funds from card payments.

Both providers offer straightforward settlement processes and easy-to-use dashboards.

The deciding factor is likely to be whether PayPal integration is important to your business.

🏆 Payouts Verdict

For businesses already using PayPal, Zettle has a clear advantage.

For everyone else, there is very little to separate the two providers.

Winner: Zettle (for PayPal users)

Overall: Tie for most businesses

Which Is Best For Your Business?

The best card payment provider depends on how your business operates, how many card payments you process and which features matter most to you.

Here’s how SumUp and Zettle compare for different types of UK businesses.

Sole Traders

Winner: SumUp

For sole traders, simplicity and affordability are usually the top priorities.

Both SumUp and Zettle are easy to set up, require no long-term contract and allow businesses to start accepting card payments quickly.

However, SumUp’s slightly lower transaction fee gives it the edge. Even small savings can add up over time, particularly for sole traders looking to keep overheads low.

Both providers offer Tap to Pay and low-cost ways to start accepting card payments. However, SumUp’s lower transaction fees make it the slightly more cost-effective option for many sole traders.

Market Traders

Winner: Tie

Both providers are well suited to market traders and mobile businesses.

They offer:

- Portable payment solutions

- Contactless payments

- Smartphone compatibility

- No monthly fee requirements

For businesses selling at markets, events and pop-up locations, either provider is likely to perform well.

The decision may come down to whether you prefer SumUp’s lower fees or Zettle’s PayPal integration.

Tradespeople

Winner: SumUp

Many tradespeople need a simple way to take card payments on-site without committing to monthly contracts.

Both SumUp and Zettle offer Tap to Pay functionality and low-cost ways to start accepting card payments. However, SumUp’s lower transaction fee gives it a slight advantage for tradespeople who regularly take card payments from customers.

This can be particularly beneficial for:

- Electricians

- Plumbers

- Builders

- Landscapers

- Mobile service businesses

The ability to accept payments directly through a compatible smartphone can be especially useful when travelling between jobs, and both providers offer this capability.

Retail Shops

Winner: SumUp

Retail businesses often need more than a basic card reader.

As sales volumes increase, requirements can include:

- Dedicated payment terminals

- Inventory management

- Point-of-sale software

- Faster checkout processes

While both providers offer suitable solutions for small retailers, SumUp provides more standalone payment device options, while Zettle offers strong retail POS and StoreKit solutions through the PayPal ecosystem.

This can reduce the likelihood of needing to switch providers later.

Cafés & Hospitality Businesses

Winner: SumUp

Cafés, coffee shops, food outlets and hospitality businesses often process a large number of lower-value transactions throughout the day.

In these situations, transaction fees become increasingly important.

SumUp’s lower standard fee can help reduce payment processing costs over time, while its broader range of payment devices provides more options for busy environments.

For growing hospitality businesses, the availability of additional hardware and software tools also provides greater flexibility.

Growing Businesses

Winner: SumUp

This is where the gap between the two providers becomes most noticeable.

Businesses experiencing growth often need:

- More advanced payment setups

- Additional payment device options

- Better scalability

- Lower transaction costs

SumUp performs strongly in all of these areas.

The availability of Payments Plus can also help larger businesses reduce card processing costs, something Zettle does not currently offer.

While Zettle remains an excellent option for small businesses, SumUp generally provides more payment device options and lower-cost processing opportunities for businesses expecting to expand.

Pros and Cons

SumUp Pros

- Lower standard transaction fee

- Optional reduced-rate pricing through Payments Plus

- More standalone payment device options

- Strong software ecosystem

- No monthly fee required

- No long-term contract

- Suitable for both small and growing businesses

SumUp Cons

- Payments Plus adds another pricing option to evaluate

- PayPal integration is not as strong as Zettle’s

- Some advanced tools may require additional subscriptions

Zettle Pros

- Simple pricing structure

- Strong PayPal integration

- Easy to set up and use

- No monthly fee required

- No long-term contract

- Well suited to small businesses and sole traders

Zettle Cons

- Slightly higher transaction fee

- No reduced-rate pricing option

- Fewer standalone payment device options

Is SumUp or Zettle Better Value?

For businesses taking only occasional card payments, there is very little between the two providers.

Both offer:

- Pay-as-you-go pricing

- No monthly contract

- Easy setup

- Reliable card payment processing

However, when looking at overall value, SumUp has several advantages.

The lower standard transaction fee means businesses pay less on every card transaction. The availability of Payments Plus creates the potential for even greater savings, particularly for businesses processing larger payment volumes.

SumUp also offers a wider range of hardware and business tools, making it easier for businesses to continue using the platform as they grow.

One of Zettle’s key differentiators is its connection to the PayPal ecosystem. Businesses already invested in the PayPal ecosystem may find this compelling enough to outweigh the differences elsewhere.

Based on pricing, SumUp provides the stronger overall value proposition.

🏆 Overall Value Winner: SumUp

Frequently Asked Questions

Is SumUp cheaper than Zettle?

Yes. SumUp charges a standard in-person transaction fee of 1.69%, compared with Zettle’s 1.75%.

While the difference is relatively small, SumUp is slightly cheaper on every card transaction and may offer greater savings over time, particularly for businesses processing larger payment volumes.

Does Zettle work with PayPal?

Yes.

Zettle is part of PayPal Point of Sale and integrates closely with the wider PayPal ecosystem. This makes it an attractive option for businesses that already use PayPal for online payments or ecommerce.

Which card reader is better, SumUp or Zettle?

Both providers offer reliable card payment solutions.

Based on pricing, SumUp is likely to be the better choice due to its lower fees and optional reduced-rate pricing. Zettle remains a strong option for businesses that value PayPal integration.

Which provider pays out faster?

Both SumUp and Zettle offer straightforward settlement processes and transfer funds directly to your linked bank account.

For most businesses, payout speed is unlikely to be the deciding factor when choosing between the two providers.

Does SumUp have lower fees than Zettle?

Yes.

SumUp’s standard in-person transaction fee is 1.69%, compared with Zettle’s 1.75%.

SumUp also offers Payments Plus, which can reduce fees on eligible domestic consumer card transactions to as little as 0.99%.

Is Zettle owned by PayPal?

Yes.

Zettle is part of PayPal Point of Sale and operates within the wider PayPal ecosystem.

Can I switch from Zettle to SumUp?

Yes.

There are no long-term contracts with either provider, so businesses can switch if they find another solution that better suits their needs.

Before switching, it’s worth comparing transaction fees, hardware requirements and software features to ensure the new provider is the right fit.

Do either SumUp or Zettle charge monthly fees?

No monthly subscription is required to start accepting card payments with either provider. Both operate primarily on a pay-as-you-go model, making them accessible to startups, sole traders and small businesses.

Final Verdict

Both SumUp and Zettle are capable card payment solutions for UK small businesses, offering simple setup, pay-as-you-go pricing and no long-term contracts.

When comparing costs, SumUp has a clear advantage. Its lower standard transaction fee and optional reduced-rate pricing through Payments Plus can help businesses reduce card processing costs, particularly as payment volumes grow.

Zettle’s main differentiator is its connection to the PayPal ecosystem. Businesses that already use PayPal may appreciate having their payment services within the same ecosystem, although the value of this will vary depending on how their business operates.

Ultimately, the choice comes down to what matters most to your business. If keeping card payment costs as low as possible is your priority, SumUp comes out ahead on pricing. If PayPal integration is particularly important to your workflow, Zettle may be worth considering.

Our Verdict

Based on pricing, SumUp offers better value thanks to its lower transaction fees and optional reduced-rate pricing. Zettle remains a strong alternative for businesses that place a high value on PayPal integration and the wider PayPal ecosystem.

View current pricing and devices:

SumUp Pricing → Zettle Pricing →Ready to Learn More?

Before making a decision, it’s worth taking a closer look at each provider’s pricing and hardware options.

Our detailed provider guides explain transaction fees, card reader costs, optional subscriptions and potential additional charges in more detail.

This can help ensure you choose the card payment provider that best fits your business today and as it grows in the future.

Related Guides

SumUp Fees UK

See our complete breakdown of SumUp pricing, transaction fees and hardware costs.

Read Guide →Zettle Fees UK

Compare Zettle’s pricing, subscription plans and payment processing costs.

Read Guide →Square vs SumUp UK

Compare two of the UK’s most popular card payment providers side-by-side.

Read Guide →Best Card Payment Machines UK

Ready to choose a provider? Compare the leading card payment machines for UK businesses.

Read Guide →Cheapest Card Readers UK

Looking for the lowest-cost option? Compare affordable card readers and fees.

Read Guide →Card Machine Fees Explained

Understand transaction fees, monthly charges and the true cost of accepting card payments.

Read Guide →